Estimating Future Discretionary Benefits Without Monte Carlo Simulation

Failed to add items

Add to basket failed.

Add to wishlist failed.

Remove from wishlist failed.

Adding to library failed

Follow podcast failed

Unfollow podcast failed

Estimating Future Discretionary Benefits Without Monte Carlo Simulation

-

Narrated by:

-

By:

About this listen

This story was originally published on HackerNoon at: https://hackernoon.com/estimating-future-discretionary-benefits-without-monte-carlo-simulation.

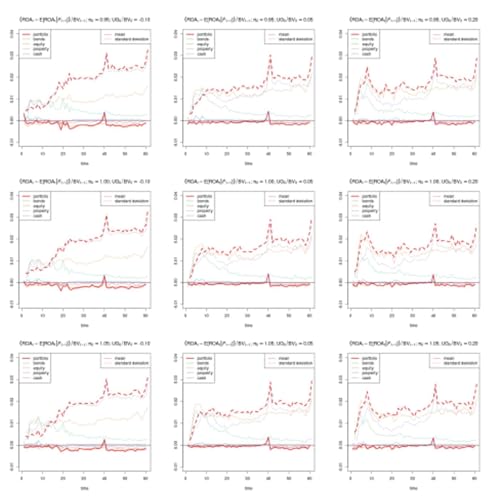

A deterministic framework for estimating future discretionary benefits in life insurance, offering tight bounds without Monte Carlo simulation.

Check more stories related to finance at: https://hackernoon.com/c/finance. You can also check exclusive content about #insurance-regulation, #market-consistent-valuation, #solvency-ii, #actuarial-modeling, #mean-field-libor-market-model, #asset-liability-management, #monte-carlo-valuation, #financial-risk-modeling, and more.

This story was written by: @solvency. Learn more about this writer by checking @solvency's about page, and for more stories, please visit hackernoon.com.

This article presents a deterministic method for estimating future discretionary benefits in life insurance portfolios by deriving stable upper and lower bounds, avoiding reliance on Monte Carlo simulations while maintaining market consistency.